“Microfinance”, every time I hear this word, only one thing hovers around my mind, i.e. high valued and highly volatile market price in stock exchange. There are many facts that microfinance scrip are attractive and has volatile market value, which is not only due to dividend they provide, also because of their performance in each quarterly report. Keeping in mind the continuous fall in price of microfinance as well as other listed companies and in overall index of Nepal Stock Exchange (NEPSE) from long time, it is our obligations to analyze the performance of the companies thoroughly, otherwise, to bear huge losses might be the only option that remains. But everyone should remember, bullish and bearish trend (up and down) are the two beautiful aspects of the market for traders. “Buy Low, Sell High” is the one and only strategy to make portfolio green but this is really hard task for every investors until and unless one analyze the major fundamentals of the companies.

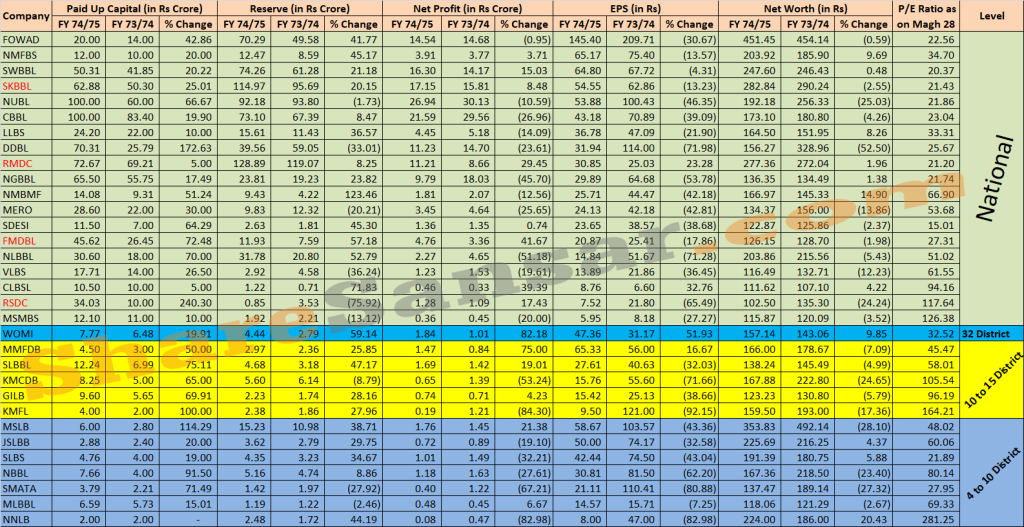

Out of 33 listed microfinance companies except Summit Microfinance Development Bank Limited (SMFDB) of Nepal have published their financial statements till the end of second quarter of the current fiscal year FY2074/75. It is the matter of interest of all the investors to analyze the important fundamentals of the microfinance companies. Thus, for an ease to investors and all visitors of our website, we have compiled a table with major fundamentals factors like paid-up capital, reserves, net profit, earnings per share (EPS), net worth per share and Price-To-Earnings ratio (P/E ratio) of Q2 of the FY 2074/75 and Q2 of the FY 2073/74 in the below table:

(Requested to download photo for clear view and further use)

Note:

(Requested to download photo for clear view and further use)

Note:

- EPS and Price Earning ratio (P/E ratio) are annualized. And to calculate P/E ratio, Closing Market Price (MP) as on Magh 28, 2074 are taken into consideration.

- Paid up capital and reserve are taken as per the unaudited report as published by the respective companies. Thus, capital of some companies may vary with the capital as listed in Nepal Stock Exchange (NEPSE).

- Table is arranged on the basis of higher to lower EPS of the respective companies under their own sector wise.

- National Level Companies with red are wholesale microfinance.

From the above table, it is concluded that out of 20 national level microfinance including 4 wholesale microfinance, Forward Community Microfinance (FOWAD) stood at the top of table with EPS and Net worth of Rs 145.40 and Rs 451.45 respectively. Its P/E ratio is also good at 22.56 times only. Likewise, RSDC Laghubitta (RSDC) and Mahila Sahayatra Microfinance (MSMBS) stood at the bottom of the table with EPS of Rs 7.52 & Rs 5.95 respectively.

Similarly, Womi Microfinance (WOMI), one and only microfinance which spreads in 32 district earns Rs 1.84 crore in the second quarter of the current FY 2074/75 as compared to Rs 1.01 crore in the corresponding quarter of the FY 2073/74. Its EPS rises by 51.93% to Rs 47.36.

Here, Mirmire Microfinance (MMFDB) with an EPS of Rs 65.33 stood at peak among 10 to 15 districts level microfinance companies. Among 5 microfinance, MMFDB is the only one microfinance whose EPS hiked by 16.67%, rest of all microfinance EPS in Q2 FY 2074/75 dwindle. Drastic fall in EPS of Kisan Microfinance from Rs 121 to Rs 9.50 pulls it to stay at the last among 10 to 15 district level microfinance.

Lastly, Charming scrip, Mahuli Laghubitta (MSLB) has EPS and net worth of Rs 58.67 & Rs 353.83 respectively. Naya Nepal having paid up capital of Rs 2 crore only posted net profit of Rs 8 lakh only in Q2 FY 2074/75. It’s EPS stood at Rs 8 which was Rs 47 in the corresponding quarter of the FY 2073/74.

In Conclusion, investors must analyze microfinance according to their working areas or levels. Comparing all ‘D’ class microfinance companies under single table might not give effective outcome as the working procedures and strategy of one another may vary which will directly result in their profit and other indicators.

.png)