Life insurance are those companies which provide sign of relief to nominees in case of death of insured or to the family of insured in case if insured suffers from major life issues. To avail Life insurance policies among Nepalese are in growing stage. Only 7-8% populations have bought life insurance policies till now, which clearly shows the life insurance market is still virgin and has high growth potentials.

Life insurance companies are the one who has been serving to the general public and also focused to gain something from the service they provide, i.e. increasing worth of the owner (shareholders) of the company.

Till the end of second quarter (Q2) of the FY 2074/75, 8 life insurance companies are listed and 7 companies’ shares are regularly traded in Nepal Stock Exchange (NEPSE). Insurance Board of Nepal (Beema Samiti) had already given license to 9 new life insurance companies and most of them have started their operation successfully. This will directly helps to cater more and more people of the nation in the web of life insurance coverage.

This article is based on the Q2 FY 2074/75 report of the 8 listed life insurance companies which will directly benefit to the investors to make necessary fundamental analysis and also to new insurance companies to build strategy to compete with the existing companies.

Below we have extracted various data from the report of Q2 FY 2074/75 as published by the respective companies in the leading newspaper:

Table 1:

Above table shows the details comparative fundamental factors of 8 life insurance companies. From the table, we can conclude that Nepal Life Insurance Company Limited (NLIC) has lead other companies in terms of highest paid up capital of Rs 3.09 arba, reserve of Rs 5.02 arba, insurance fund of Rs 45.63 arba, contingent fund of Rs 32.53 crore and net profit of Rs 27.96 crore. NLIC is followed by National Life insurance whose net profit amounts to Rs 17.08 crore inclined from Rs 8.51 crore in the Q2 FY 2073/74.

Those insurance companies listed above must hike their paid up capital to Rs 2 arba till the end of Ashad 2075 as directed by the Insurance Board of Nepal. For which most of the companies have published their

capital plans. (Click to see the capital plan)

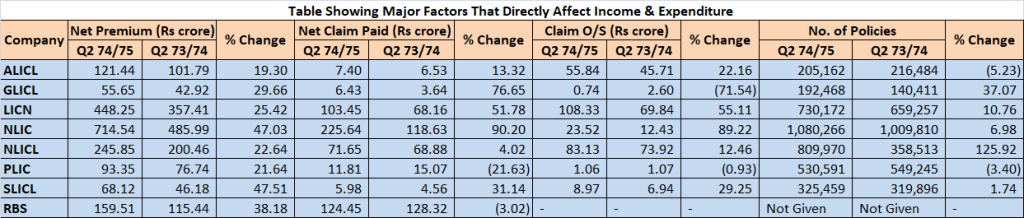

Table 2:

Above table gives us an idea related to the vital factors that affects the profit and expenses including business of the insurance companies. Here also, Nepal Life Insurance(NLIC) has shown the strong base behind the highest net profit due to accumulation of 10.80 lakh unit polices. It has collected Rs 7.14 arba as net premium and paid claims of Rs 2.25 arba. It is followed by Life Insurance Corporation Nepal (LICN) with Rs 4.48 arba of premium collection and Rastriya Beema Sansthan (RBS) with Rs 1.59 arba. Surya Life Insurance (SLICL) and NLICL succeed to hike their net premium by around 47% which is highest among all 8 companies. LICN has outstanding claim of Rs 1.08 arba but this amount need not to be borne solely by LICN, majorportion of this will be borne by Re- Insurance companies which makes the company from the fear of equity hit and secure the company’s shareholder wealth.

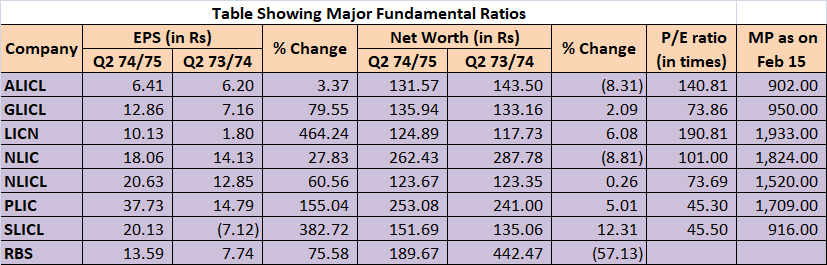

Table 3:

And at last, Table 3 might be the best one to make fundamental analysis to the investors as this table solely includes major 3 fundamental ratios. In terms of EPS, Prime Life Insurance (PLIC) came at first among other companies with EPS of Rs 37.73 which is only Rs 14.79 at the end of Q2 FY 2073/74. But NLIC has highest net worth per share of Rs 262.43 followed by PLIC with net worth per share of Rs 253.08. Those investors who make fundamental analysis in terms of Price Earning ratio (P/E ratio), PLIC and SLICL would be the best buy as it has only P/E ratio of 45 times. P/E ratio of LICN is massive at 190.81 times.(

Note: Earning from actuary valuation is not included while calculating above major ratio. So the above ratio might differ once the amount from actuary valuation included on Profit and loss Account. The companies with highest life insurance fund have higher chance to get more amounts under this heading after the end of fiscal year.)

.png)