Exploring Intrinsic Value - A look at Shivam Cements Limited

Thu, Dec 22, 2022 1:56 PM on Stock Market, Recommended, Exclusive,

VALUING SHIVAM CEMENT LTD (SHIVM)

Shivam Cement Ltd, founded in 2003, is one of Nepal’s largest cement manufacturers. It has its factory in Hetauda and owns its own limestone quarry. (More about the company here: https://shivamcement.com.np/page/introduction)

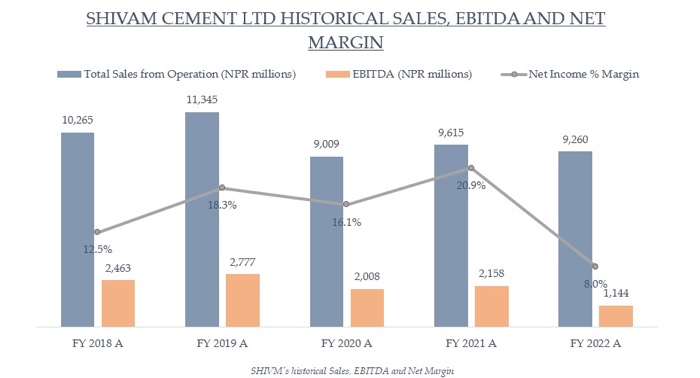

The company’s sales have declined marginally in recent years primarily due to a lack of customer demand caused by the pandemic. Alarmingly, the company’s profitability has seen a significant drop in FY 2022. Its net income margin declined from 20.9% in FY 2021 to 8% in FY 2022. This was due to increases in the cost of raw materials and inputs.

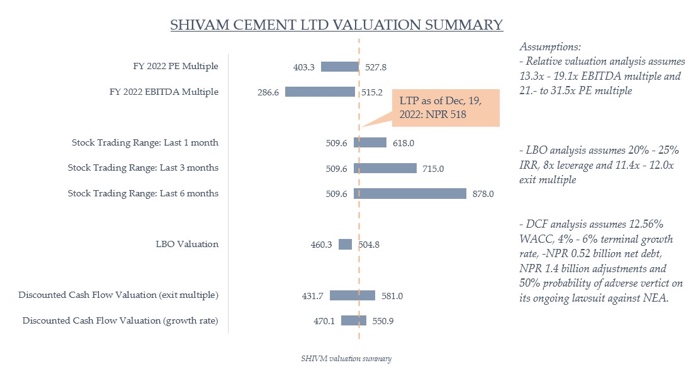

The figure below provides a summary of SHIVM’s values calculated using various methods as of December 19, 2022.

Based on the various valuation analysis, details of which are presented below, SHIVM is currently trading within its intrinsic value limits.

DISCOUNTED CASHFLOW ANALYSIS

The following discounted cash flow analysis is based on the assumption that the company can grow sales, and profitability back to its pre-pandemic levels within the next 5 years. More aggressive growth in sales and profitability is unlikely given the current macroeconomic condition and intense competition in the industry.

Using a risk-free rate of 4.47%, a market risk premium of 9.77%, and a beta of 1.0 yields a cost of equity of 14.24%. Similarly, a 13% interest on long-term debt and a 25% tax rate gives a cost of debt of 9.75%. Thus, with the company’s current capital structure, its Weighted Average Cost of Capital (WACC) is 14.12%.

A normalized WACC based on the sector average debt-to-equity ratio is 12.56%. This DCF analysis assumes the company will take steps to optimize its capital structure and reduce its cost of capital from its current 14.12% to 12.56% linearly over the next 5 years.

A quick look at the company’s Beta before moving forward. SHIVM’s regression beta is very erratic and ranges from 0.45 (last 2 years) to 2.12 (last 3 months).

A bottom-up Beta calculation did not prove fruitful because of a lack of usable data. There are very few directly comparable companies with relevant data in Nepal.

A Beta of 1.0 has been used for this analysis. For reference, the average regression Beta for similar industries internationally is 1.14.

The enterprise value of the company using a perpetual growth rate of 4.5% and WACC of 12.56% is NPR 19.2 billion. Adjusting for Net Debt, Holdings, and a 50% possibility of adverse judgment on a significant lawsuit filed against the company by the Nepal Electricity Authority, the implied share price for SHIVM is NPR 505.5.

The table below shows SHIVM’s implied share prices based on different discount rates and growth rates.

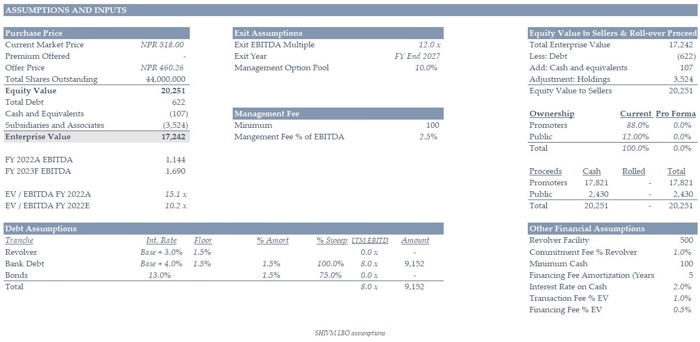

LBO ANALYSIS

The Leveraged Buy-Out (LBO) valuation method provides further insights into the company’s value from a private equity perspective.

With standard LBO assumptions of leverage, management, and other fees, combined with Nepal’s current interest rate environment and an expected IRR between 20% and 25% for the sponsors, the possible offer prices for SHIVM range between NPR 460 and NPR 505 per share.

The table below summarizes the various returns possible under different offer prices and leverage scenarios.

RELATIVE VALUATION

There are currently 6 manufacturing and processing companies listed in Nepal Stock Exchange, of which Shivam Cement Ltd is the only cement-producing company.

SHIVM’s implied share price ranges between NPR 286 and NPR 515 based on historical EBITDA multiples for the sector and between NPR 403 and NPR 527 based on the historical Price/Earnings ratio for the sector.

As of December 2022, the company’s shares are trading between NPR 518 and NPR 600 per share. This price range implies that the market is assuming the company can achieve an annual revenue growth rate of 5% to 7% and an annual increase in EBITDA margin between 2.5% and 3.5% for the next 5 years.

(Disclaimer: DO NOT consider views expressed above as investment advice. Conduct your own due diligence before investing.)

About the Author:

Nischay Shrestha has an MBA specializing in Corporate Finance and Investment Banking from the Wisconsin School of Business, University of Wisconsin Madison.